Assessing Your Financial Readiness and Building Your Down Payment

Before you start browsing listings, every first-time condo buyer in Toronto needs to take an honest look at their financial picture. Begin by calculating your Gross Debt Service (GDS) and Total Debt Service (TDS) ratios, which lenders use to determine how much you can realistically borrow. Meeting with a mortgage broker or your bank early in the process gives you a clear picture of your borrowing power and prevents the heartbreak of falling in love with a unit you cannot afford. Your condo down payment represents the largest upfront expense, and building it requires strategic discipline. Open a First Home Savings Account (FHSA) immediately to maximize contribution limits and tax benefits. Meanwhile, audit your monthly spending ruthlessly, cancel unused subscriptions, brew your coffee at home, and try short no-spend challenges. With Toronto condo affordability improving thanks to current market softness, your savings target may be more achievable than you think.

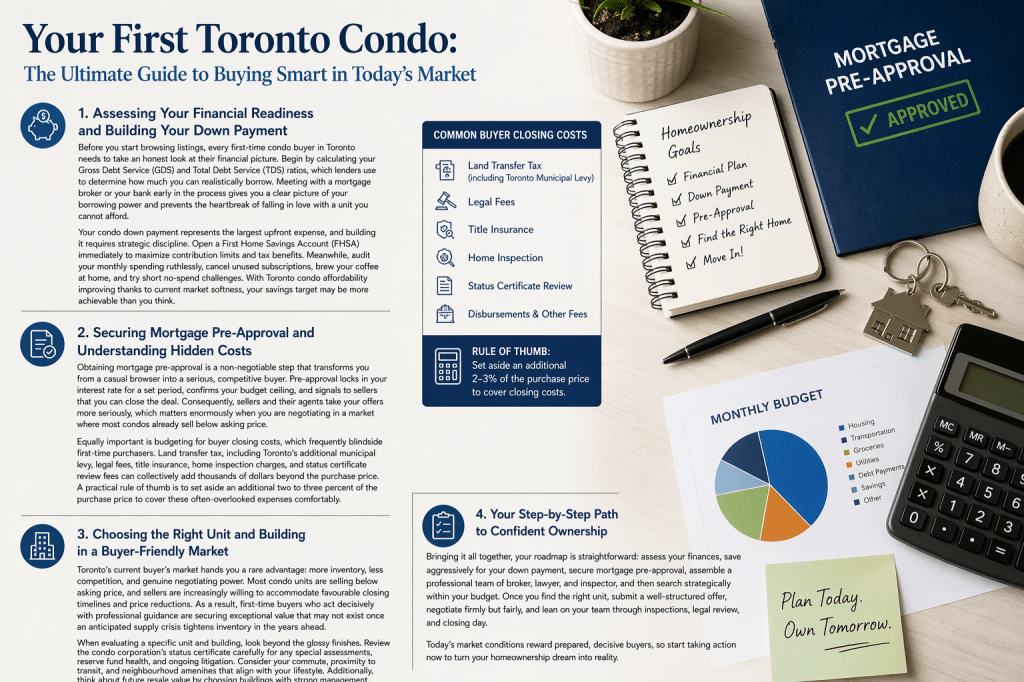

Securing Mortgage Pre-Approval and Understanding Hidden Costs

Obtaining mortgage pre-approval is a non-negotiable step that transforms you from a casual browser into a serious, competitive buyer. Pre-approval locks in your interest rate for a set period, confirms your budget ceiling, and signals to sellers that you can close the deal. Consequently, sellers and their agents take your offers more seriously, which matters enormously when you are negotiating in a market where most condos already sell below asking price. Equally important is budgeting for buyer closing costs, which frequently blindside first-time purchasers. Land transfer tax, including Toronto’s additional municipal levy, legal fees, title insurance, home inspection charges, and status certificate review fees can collectively add thousands of dollars beyond the purchase price. A practical rule of thumb is to set aside an additional two to three percent of the purchase price to cover these often-overlooked expenses comfortably.

Choosing the Right Unit and Building in a Buyer-Friendly Market

Toronto’s current buyer’s market hands you a rare advantage: more inventory, less competition, and genuine negotiating power. Most condo units are selling below asking price, and sellers are increasingly willing to accommodate favourable closing timelines and price reductions. As a result, first-time buyers who act decisively with professional guidance are securing exceptional value that may not exist once an anticipated supply crisis tightens inventory in the years ahead. When evaluating a specific unit and building, look beyond the glossy finishes. Review the condo corporation’s status certificate carefully for any special assessments, reserve fund health, and ongoing litigation. Consider your commute, proximity to transit, and neighbourhood amenities that align with your lifestyle. Additionally, think about future resale value by choosing buildings with strong management, low vacancy rates, and well-maintained common areas.

Your Step-by-Step Path to Confident Ownership

Bringing it all together, your roadmap is straightforward: assess your finances, save aggressively for your down payment, secure mortgage pre-approval, assemble a professional team of broker, lawyer, and inspector, and then search strategically within your budget. Once you find the right unit, submit a well-structured offer, negotiate firmly but fairly, and lean on your team through inspections, legal review, and closing day. Today’s market conditions reward prepared, decisive buyers, so start taking action now to turn your homeownership dream into reality.