Buying your first home is one of the most significant financial decisions most people will make in their lifetime, and doing it in a market like Mississauga City Centre comes with a specific set of considerations that go well beyond what the standard first-time buyer guides will tell you. I have been working with first-time buyers across the GTA for over two decades, and I can tell you honestly that the buyers who come to the process informed, with clear expectations and a solid understanding of their financial position, consistently have better outcomes than those who learn on the fly. The current market, with its elevated inventory, negotiable sellers, and moderating prices, is genuinely one of the more favourable entry environments for first-time buyers that I have seen in years. Let me walk you through what you need to know to approach this market well.

Getting Your Financing Right Before You Start Looking

The single most important step any first-time buyer can take before looking at a single listing is to get a thorough mortgage pre-approval and to understand, clearly, what their Gross Debt Service (GDS) and Total Debt Service (TDS) ratios look like across different purchase price scenarios. These ratios determine how much mortgage a lender will approve, and understanding them helps you set a realistic budget rather than relying on online calculators that may not reflect your complete financial picture. Your GDS should generally not exceed 39% of your gross income, and your TDS should not exceed 44%, though lenders use these as guidelines rather than absolute cut-offs. Knowing your numbers going in prevents the disappointment of falling in love with a unit that is beyond your actual purchase capacity.

First-time buyers in Canada have access to two meaningful government programmes worth understanding thoroughly. The First Home Savings Account (FHSA) allows eligible buyers to contribute up to a set annual limit and accumulate tax-sheltered savings specifically for a first home purchase, with contributions being tax-deductible and withdrawals for qualifying purchases being tax-free. The RRSP Home Buyers’ Plan allows first-time buyers to withdraw a significant sum from their RRSP tax-free for a home purchase, subject to repayment over 15 years. Using both strategically can meaningfully increase your effective down payment, particularly if you have been saving for a few years. I always recommend working with a mortgage professional and a financial planner alongside your realtor to ensure you are maximising these tools before your purchase.

Why City Centre Is Particularly Well-Suited for First-Time Buyers

Mississauga City Centre offers a combination of attributes that makes it genuinely well-suited for first-time condo buyers. Entry-level prices are more accessible than comparable urban Toronto locations, the walkable amenities reduce the transportation costs that often accompany suburban living, and the improving transit network means that owning a car, while still convenient, is less essential than in most GTA suburban areas. For buyers who are moving from a rental situation to ownership, the City Centre lifestyle is often a relatively seamless transition because the walkability and access to services they valued as renters is maintained, or even improved, as owners. In my view, this makes the neighbourhood an excellent first step on the property ladder for buyers who want to maintain an urban lifestyle without paying Toronto prices.

In my daily practice, I am seeing more first-time buyers actively choosing City Centre over the alternatives precisely because of this value proposition. The current buyer’s market amplifies the appeal: sellers are negotiating, conditions are accepted, and buyers have the time to do proper due diligence on status certificates and building financials rather than being rushed into unconditional offers. I cover more about how the neighbourhood’s fundamentals benefit buyers of all experience levels in my comprehensive Mississauga City Centre guide, which I keep updated with current market observations.

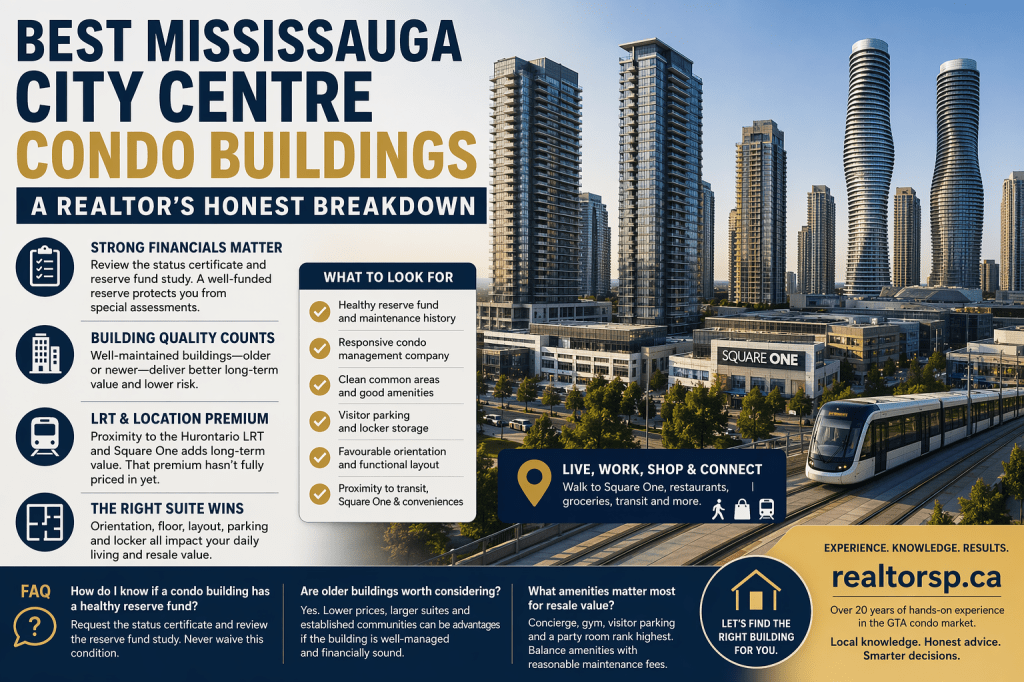

The Status Certificate: Your Most Important Due Diligence Step

First-time condo buyers are often unfamiliar with the status certificate process, and I want to be direct about its importance: reviewing the status certificate before finalising any condo purchase is not optional. The status certificate is a package of documents from the condo corporation that includes the current reserve fund balance and adequacy study, recent meeting minutes, the budget, any outstanding special assessments or legal disputes, and the rules of the condo corporation. Your real estate lawyer will review this document and flag anything material, but as a buyer you should also read the meeting minutes yourself to get a sense of the building’s ongoing issues and the quality of its governance. Buildings where minutes reflect chronic complaints about the same unresolved issues, or where the reserve fund study shows significant underfunding relative to projected capital needs, are buildings to approach with caution regardless of how attractive the unit itself may be.

As a real estate professional with over 20+ years of experience in the industry, I have first-hand witnessed buyers who waived the status certificate review in competitive markets and later discovered serious financial issues within the corporation. In today’s market, where there is no competitive pressure to forgo conditions, there is absolutely no reason to skip this step. Make it a condition of every offer, give yourself the full review period allowed, and take the results seriously. A building with a strong status certificate is worth more than a building with a cheap sticker price and hidden liabilities.

Frequently Asked Questions from First-Time Condo Buyers in City Centre

How much do I need for a down payment on a City Centre condo?

In Canada, the minimum down payment for homes under a set price threshold is 5% of the purchase price, with a sliding scale for higher-priced properties. On a condo in the City Centre price range, that minimum is attainable for many first-time buyers, especially when combined with FHSA and RRSP Home Buyers’ Plan withdrawals. Putting more down reduces your mortgage insurance premium and monthly carrying costs, so it is worth building savings beyond the minimum if possible.

What are the closing costs first-time condo buyers should budget for?

Typical closing costs include land transfer tax (first-time buyers receive a provincial rebate in Ontario and a municipal rebate in some cities), legal fees, title insurance, and any adjustments for property tax or maintenance fees prepaid by the seller. Budget roughly 1.5% to 2% of the purchase price for these costs on top of your down payment to avoid any surprises at closing.

Can a first-time buyer negotiate effectively in the City Centre market?

Yes, and more so than at any point in recent memory. The current buyer’s market gives first-time purchasers the ability to include conditions, negotiate on price, and take the time for proper due diligence. This is a genuine structural advantage compared to the multiple-offer environment that prevailed in 2021 and 2022. Working with an experienced realtor who understands the local market is critical to negotiating effectively.

Your First Step Onto the Property Ladder

Buying your first condo in Mississauga City Centre in 2026 is a realistic goal for many buyers who have been preparing financially, and the current market conditions make the process less stressful and more buyer-friendly than it has been in years. The key is approaching the process with solid financial preparation, a clear understanding of what you are buying (including the condo corporation’s financial health), and the patience to find the right unit rather than rushing into the first thing that looks acceptable. This neighbourhood rewards buyers who take the time to understand it.

Building Your Long-Term Equity from Day One

For first-time buyers, the purchase of a City Centre condo is not just a housing decision; it is the foundation of a long-term wealth-building strategy. Every mortgage payment made on a property you own builds equity that renting never would. The appreciation potential of a well-chosen City Centre unit over a five-to-ten-year holding period has historically been meaningful, and the current entry conditions make the starting point more favourable than it has been in several years. Buyers who purchase thoughtfully in 2026, with solid due diligence and realistic expectations about the near-term market, are positioning themselves to benefit from the longer-term appreciation story that the neighbourhood’s fundamentals support. The first step on the property ladder is often the most important one, and in my experience, the clients who made that first purchase even when conditions felt uncertain are consistently the ones who are most grateful for having done so when they look back several years later.

I work with first-time buyers throughout the GTA and take genuine satisfaction in helping people navigate this process well. If you are considering your first purchase in Mississauga City Centre, visit realtorsp.ca and reach out. With over 20 years of experience guiding buyers from pre-approval to closing, I can make sure your first purchase is a well-informed one.

#FirstTimeBuyer #MississaugaCondo #FHSA #RRSPHomeBuyersPlan #GTARealEstate #MississaugaCityCenter #CondoBuying #SPSinghAhluwalia #BuyersMarket #FirstHome